In an age where technology and finance intertwine like never before, the landscape of lending is undergoing a profound transformation. Gone are the days when securing a loan required endless paperwork and in-person meetings with lenders. The rise of digital platforms, innovative fintech solutions, and data-driven decision-making is revolutionizing how borrowers and lenders interact. This article delves into the waves of disruption reshaping the lending industry, exploring how emerging technologies, shifting consumer expectations, and regulatory changes are not just reshaping access to credit but redefining the very essence of finance itself. Join us as we navigate the intricate web of change that is modernizing lending practices and what this means for the future of finance.

The Rise of Fintech Platforms and Their Impact on Traditional Lending

The emergence of fintech platforms has drastically transformed the landscape of lending, presenting both opportunities and challenges for traditional financial institutions. These platforms leverage technology to enhance customer experience, streamline processes, and offer personalized financial products at a speed that traditional lenders often struggle to match. For instance, a few standout features of fintech solutions include:

- Automated underwriting: Utilizing artificial intelligence and big data to assess credit risk quickly and accurately.

- User-friendly interfaces: Offering seamless application processes through mobile apps and websites that cater to tech-savvy borrowers.

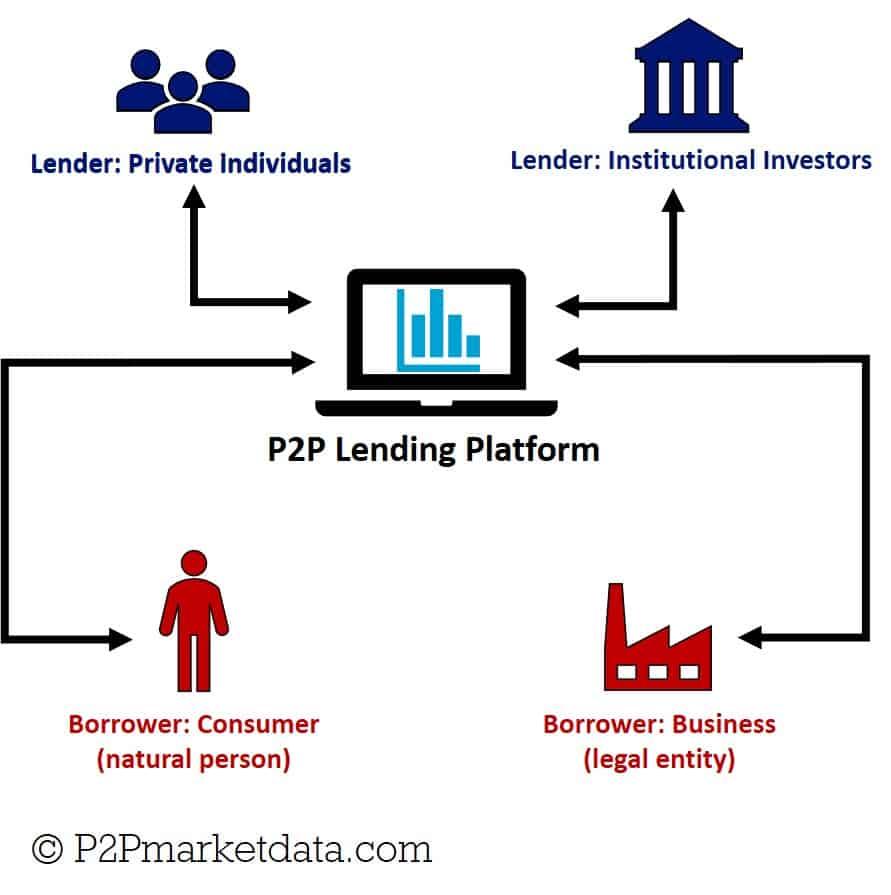

- Peer-to-peer lending: Connecting borrowers directly with investors, reducing the need for intermediaries and often resulting in lower interest rates.

As these platforms gain traction, they are compelling traditional lenders to rethink their strategies. The adaptability and innovation showcased by fintech companies serve as a catalyst for change, prompting established banks to invest in technological advancements. This has led to a more competitive market, evident through the following trends:

| Trend | Description |

|---|---|

| Collaboration | Traditional banks are partnering with fintechs for technology and expertise. |

| Digital transformation | Investing in technology to improve service delivery and customer engagement. |

| Data analytics | Utilizing customer data to enhance lending decisions and risk assessment. |

Understanding the Role of Data Analytics in Modern Credit Assessments

In today’s finance landscape, the integration of data analytics has revolutionized how lenders assess creditworthiness. Traditional methods often relied on rigid metrics and historical data, limiting the ability to capture a borrower’s true financial health. However, the advent of advanced analytics tools enables financial institutions to harness vast amounts of real-time data, providing a more nuanced view of each applicant. With the power of machine learning and artificial intelligence, lenders can analyze various factors, including:

- Alternative Data: Non-traditional sources such as social media activity and online purchasing behavior.

- Behavioral Insights: Patterns in spending and saving that predict future credit risk.

- Demographic Trends: Augmenting traditional credit scores with insights into economic conditions affecting specific populations.

Furthermore, leveraging data analytics not only enhances accuracy in credit assessments but also expedites the decision-making process. Automated algorithms can evaluate applications rapidly, reducing the time borrowers wait for approvals. This efficiency is particularly critical in a digital-first world, where customer expectations for prompt service are paramount. The following table illustrates some key benefits of implementing data analytics in credit assessments:

| Benefit | Description |

|---|---|

| Enhanced Accuracy | Improved prediction models reduce default rates. |

| Faster Processing | Automated systems speed up lending decisions. |

| Personalized Offers | Custom loan products based on individual risk profiles. |

Exploring Regulatory Challenges and Opportunities in a Changing Landscape

The rapid evolution of technology in the financial sector has introduced a myriad of regulatory challenges that demand careful navigation. As new players emerge, traditional financial institutions are compelled to rethink compliance frameworks amidst the rise of decentralized finance (DeFi) and peer-to-peer lending. Consequently, the dynamic regulatory environment presents not only obstacles but also opportunities for innovation in risk management and consumer protection. Key challenges include:

- Data Privacy and Security: Ensuring robust protection for consumer data while fostering transparency.

- Regulatory Compliance: Balancing innovation with adherence to existing laws and evolving regulations.

- Global Standards: Navigating the complexities of differing regulations across jurisdictions.

Conversely, embracing these challenges can lead to forward-thinking solutions that reshape the lending landscape. Financial institutions now have the chance to leverage technology to improve regulatory compliance through advanced analytics and automated reporting tools. Additionally, collaboration between regulators and fintech firms can unlock pathways for regulatory sandboxes, which allow for testing innovative solutions in a controlled environment. The potential impacts are significant:

| Impact | Examples |

|---|---|

| Improved Consumer Trust | Greater transparency in lending practices |

| Increased Financial Inclusion | Access to credit for underserved populations |

| Enhanced Efficiency | Reduced compliance costs through automation |

Strategies for Traditional Lenders to Adapt and Thrive in the Digital Age

In a landscape where fintech innovations redefine consumer expectations, traditional lenders must reinvent their operational frameworks and service offerings. Integrating technology into daily operations is no longer optional but essential. Lenders can start by adopting robust customer relationship management (CRM) systems to enhance personalization and engagement. Employing data analytics will enable lenders to better understand customer behaviors, improving decision-making processes. Here are some strategies for achieving this transformation:

- Embrace Automation: Streamlining application processes and loan origination through automated systems can reduce operational costs and minimize human error.

- Develop Mobile Platforms: Investing in mobile-friendly applications ensures a seamless experience for customers who prefer managing their finances on-the-go.

- Utilize Alternative Credit Scoring: Incorporating non-traditional data sources for credit assessments can broaden access to loans for underbanked populations.

Collaboration is another key strategy to stay competitive in the rapidly evolving financial ecosystem. Traditional lenders should explore partnerships with fintech startups, ensuring a synergistic approach to technology adoption. A hybrid model that combines the strengths of traditional lending with the speed and agility of fintech solutions can help mitigate risks and engage a larger customer base. The following table illustrates potential partnerships that can enhance product offerings:

| Partnership Type | Potential Benefits |

|---|---|

| Payment Processors | Faster transaction solutions and enhanced security features. |

| Credit Assessment Platforms | Improved risk assessment and faster approvals. |

| Peer-to-Peer (P2P) Lending Platforms | Access to a broader range of consumers and diversified funding sources. |

To Wrap It Up

as we stand on the threshold of a new era in finance, it becomes increasingly clear that the disruptions redefining lending are not merely transient fluctuations, but powerful catalysts for long-term change. From innovative technologies reshaping the way consumers and businesses access capital to a growing emphasis on sustainability and inclusivity, the landscape of lending is evolving at an unprecedented pace.

The financial institutions that adapt and embrace these transformations will not only survive but also thrive in this dynamic environment. Just as the compass guides explorers through uncharted waters, so too do these innovations offer pathways toward a more efficient, equitable, and transparent financial system. As we move forward, we must remain vigilant and open-minded, ready to harness the potential of these advancements while ensuring that the essence of responsible lending is not lost amidst the waves of change.

The journey of transformation is continuous, and as stakeholders in this landscape, it is our collective responsibility to foster a future where lending serves as a bridge, connecting dreams to reality, aspirations to achievements, and communities to opportunities. The future of finance is here; let us navigate it wisely.