As digital transactions continue to redefine the landscape of finance, the European Union stands at the forefront of this evolution with the impending arrival of the Payment Services Directive 3 (PSD3). Building on the foundations set by its predecessors, PSD3 promises not only to enhance the security and efficiency of electronic payments but also to usher in a new era of open banking that prioritizes innovation and consumer empowerment. In an age where seamless financial interactions are becoming the norm, this new directive aims to balance regulatory oversight with the nimbleness required to fuel competition and technological advancement. As we delve into the intricacies of PSD3, we explore how this legislation will reshape the way we manage our money, interact with financial institutions, and navigate the digital economy, paving the way for a more integrated and user-friendly ecosystem for all.

Shaping the Future of Payments: Understanding the Core Principles of PSD3

Understanding the essence of PSD3 is pivotal as it shapes a new landscape for digital transactions and open banking across Europe. Building on the foundations laid by its predecessors, this directive emphasizes enhanced consumer protection, innovation, and collaboration among financial institutions. Key principles driving PSD3 include:

- Inclusivity: Ensuring all consumers, regardless of technology access or banking experience, can engage in a seamless payment ecosystem.

- Security: Strengthening measures against fraud and enhancing the security of online payments with advanced authentication techniques.

- Transparency: Promoting clear communication around fees, terms, and conditions associated with financial services.

Another crucial aspect of PSD3 is its focus on interoperability, which facilitates greater integration among payment systems. By pushing for common standards, this directive nurtures a competitive environment that benefits both consumers and businesses. A summary of its pivotal elements illustrates this shift:

| Element | Description |

|---|---|

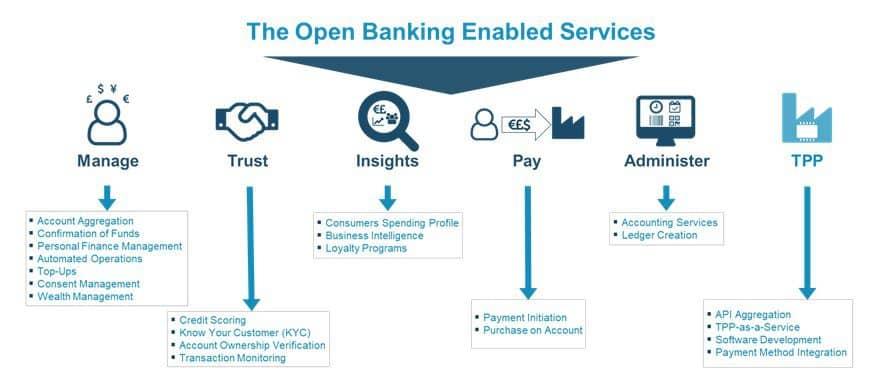

| Open Access | Framework for third-party providers to access banking infrastructure, fostering innovation. |

| Consumer Empowerment | New rights for consumers to manage their data and choice of service providers. |

| Cross-Border Transactions | Simplified processes for payments within the EU, enhancing cross-border commerce. |

Empowering Consumers: How PSD3 Enhances Transparency and Choice

The third iteration of the Payment Services Directive (PSD3) revolutionizes the European payment landscape by significantly elevating consumer rights and fostering a transparent environment. With a renewed focus on data access and interoperability, consumers can now directly link their bank accounts with multiple financial service providers. This shift not only makes it easier for individuals to compare services but also enhances competition among providers, ultimately driving down costs. The directive empowers users to seamlessly switch between different services, ensuring they receive the best value for their transactions.

Furthermore, PSD3 introduces stringent regulations on how financial institutions handle customer data, aligning with the general trend toward data privacy and protection. This regulatory framework includes provisions that require clear consent mechanisms, allowing consumers to control who accesses their data and under what circumstances. As a result, customers can enjoy a fuller spectrum of choices without the nagging worry of misuse or exploitation of their financial information. In this new landscape, transparency will reign supreme, making informed decision-making the norm rather than the exception.

Navigating the Open Banking Landscape: Opportunities and Challenges for Financial Institutions

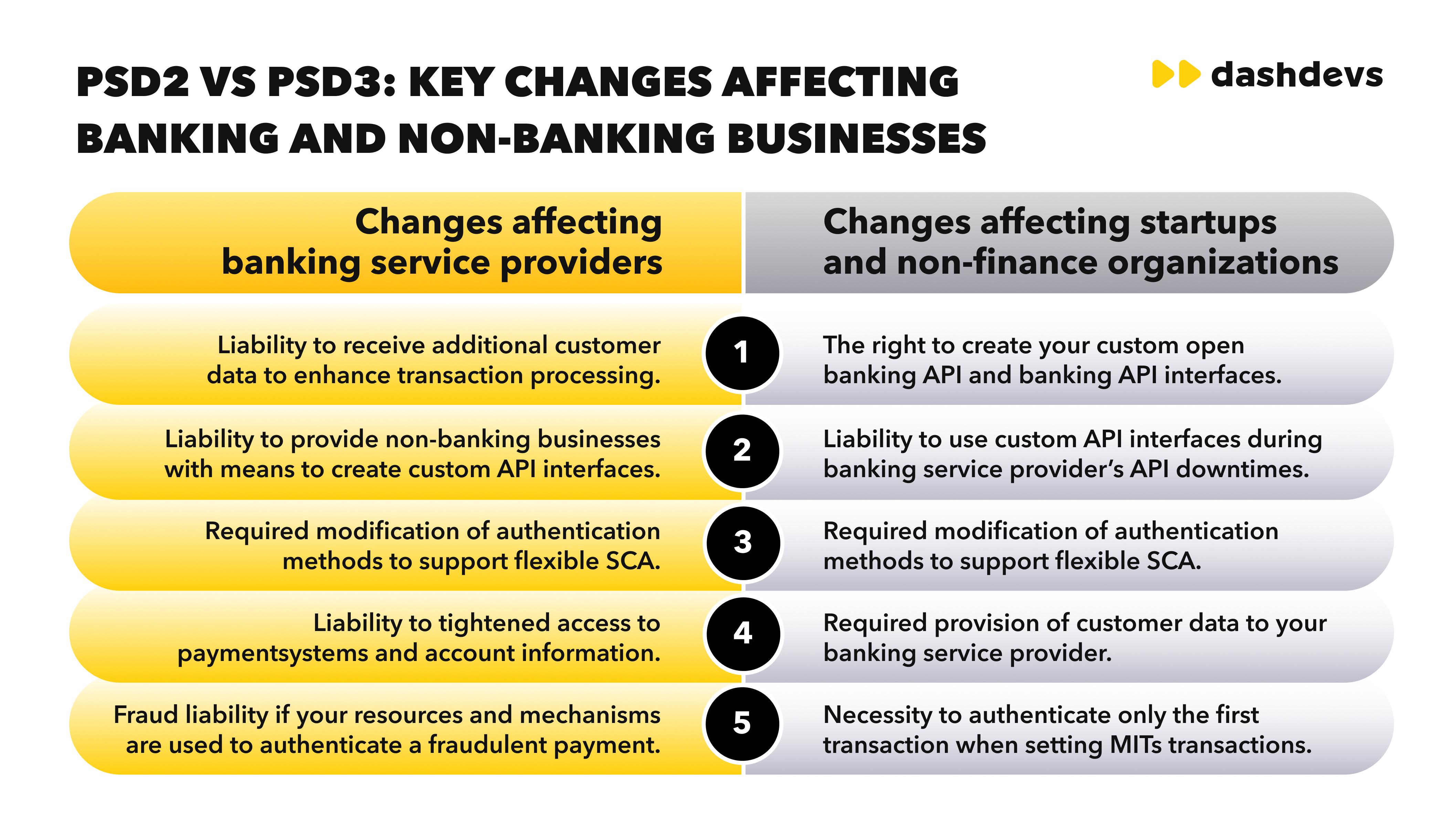

As the European Union marches towards the implementation of PSD3, financial institutions stand at a pivotal juncture. This new regulation is expected to further enhance the open banking framework established by its predecessor, PSD2, opening a plethora of opportunities. Among these, institutions can look forward to:

- Increased Collaboration: Fostering partnerships with fintechs to innovate new services.

- Enhanced Consumer Trust: Improved security measures leading to better customer confidence in digital transactions.

- Broader Access to Customer Data: Empowering banks to harness insights from customer behavior.

Yet, with each opportunity comes significant challenges that cannot be overlooked. The complexities of compliance with updated regulations may burden smaller institutions that lack the resources of their larger counterparts. Moreover, the risks associated with data privacy and cybersecurity can pose existential threats. Key challenges include:

- Navigating Regulatory Changes: Keeping up with evolving compliance standards.

- Developing Secure Platforms: Investing in robust security frameworks to protect sensitive customer information.

- Staying Competitive: Innovating continuously in a rapidly changing landscape while managing operational costs.

Strategic Recommendations for Adapting to PSD3: Embracing Innovation and Compliance

As the landscape of payments and open banking transforms with the introduction of PSD3, businesses must adopt a proactive approach to seamlessly integrate innovation while ensuring compliance. An effective strategy hinges on understanding and leveraging the new regulations. Companies should invest in robust compliance frameworks that not only adhere to PSD3 requirements but also enhance customer trust. Key strategies include:

- Conducting a comprehensive impact assessment to identify changes required within operational processes.

- Embracing cutting-edge technology, such as artificial intelligence and blockchain, to enhance transaction speed, security, and user experience.

- Fostering partnerships with fintechs and other innovators to develop collaborative solutions that align with PSD3 capabilities.

In addition to technology and partnerships, organizations should prioritize customer education and engagement. By crafting tailored communication strategies that elucidate the benefits of new payment solutions under PSD3, businesses can cultivate a loyal customer base. A focus on building transparency in data usage will further empower users and encourage the adoption of innovative services. Consider implementing:

- Interactive online platforms that offer insights into transaction management and security measures.

- Webinars and workshops to guide customers through the changes brought by PSD3.

- Feedback loops to continually refine offerings based on customer insights and preferences.

To Conclude

As we stand on the cusp of a new era in European finance, the advent of PSD3 heralds a transformative phase for both consumers and businesses alike. By reinforcing the principles of open banking and enhancing the security and efficiency of payment systems, this directive serves as a beacon for innovation and collaboration in the financial sector. As we embrace these changes, it’s essential to consider not just the new opportunities that PSD3 brings, but also the responsibilities it entails for stakeholders across the board. The road ahead is paved with potential, and as we navigate this evolving landscape, our commitment to adaptation and engagement will ultimately shape the future of payments and financial interactions in the EU. Let us prepare to embrace this change, fostering a vibrant ecosystem that empowers users and paves the way for a seamless financial experience. The journey towards a more integrated and consumer-centered financial landscape has begun; the question now is: how will we choose to embark on it?