In an increasingly digital world, the way we manage our finances is rapidly evolving, with Buy Now Pay Later (BNPL) services emerging as a popular payment option. As consumers embrace the flexibility and convenience these platforms provide, a seismic shift is occurring within the financial landscape, prompting regulators to step in and consider how these services intersect with traditional banking practices. In the UK, where the popularity of BNPL has surged, the call for regulation has intensified, leaving banks to navigate an uncharted territory filled with both challenges and opportunities. This article delves into the implications of potential BNPL regulations on the future of UK banks, examining how they can adapt to maintain relevance in a market that is being reshaped by consumer preferences, technological advancements, and an evolving regulatory framework. As we explore this complex interplay, we uncover not just the risks, but also the potential pathways for innovation and growth within the banking sector.

Understanding the Landscape: The Rise of BNPL and Its Implications for UK Banking

As the popularity of Buy Now, Pay Later (BNPL) services surges in the UK, financial institutions are faced with both opportunities and challenges that reshape the banking landscape. BNPL has emerged as a go-to solution for consumers seeking flexibility in payments, particularly among younger demographics who favor instant gratification and minimal financial friction. This trend presents an opportunity for banks to innovate their offerings, integrating BNPL solutions into their existing frameworks to attract a broader customer base. Consequently, traditional institutions must evaluate their role in this evolving marketplace, considering partnerships with BNPL providers or developing proprietary services that align with consumer demand.

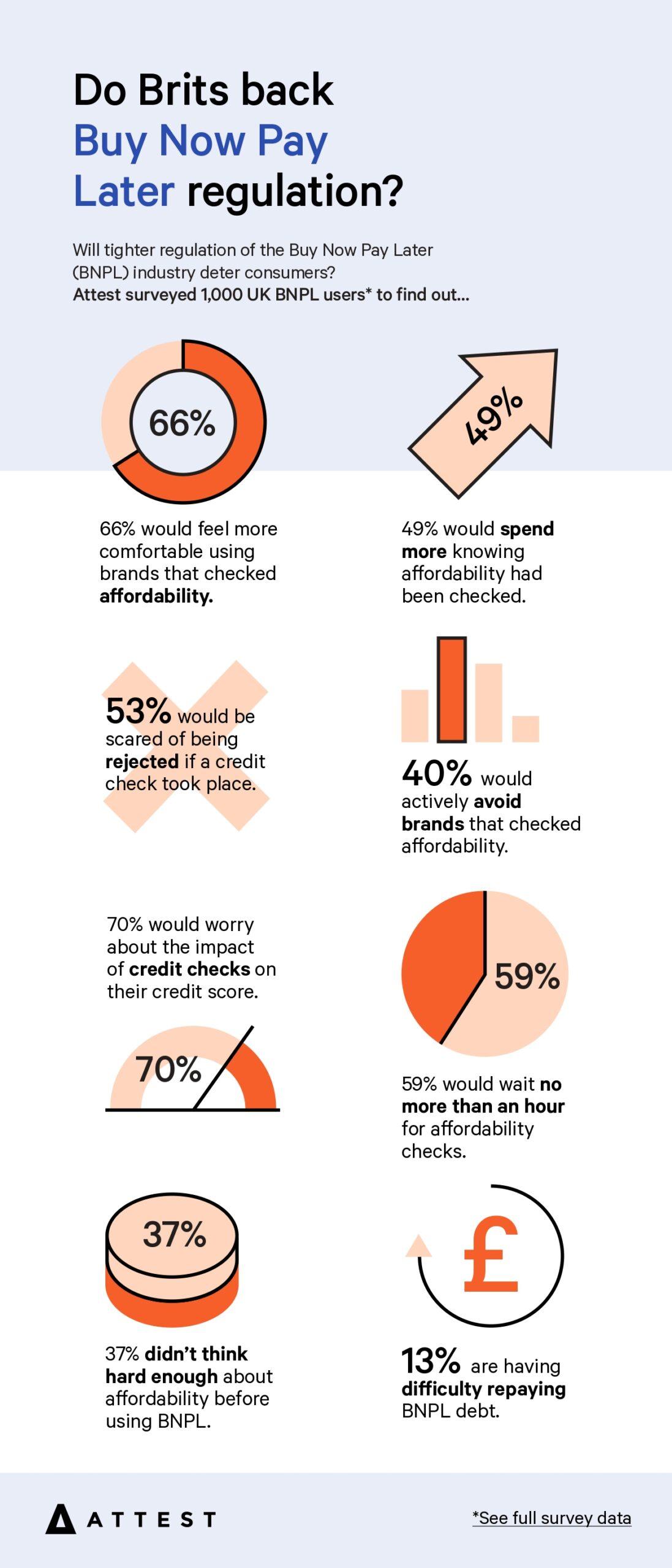

However, the rapid rise of BNPL services is not without its risks, particularly concerning regulatory scrutiny. The UK government has begun to pay closer attention to the implications of BNPL on consumer debt and financial education. Lawmakers are advocating for clearer regulations that ensure transparency and consumer protection, emphasizing the need for fair lending practices. As a result, banks must prepare to adapt to these regulatory changes by enhancing their risk assessment processes and improving disclosures related to repayment terms. The potential for a regulatory framework may be summarized as follows:

| Regulatory Focus | Implications for BNPL |

|---|---|

| Consumer Protection | Enhanced rights for consumers regarding repayment terms. |

| Transparency | Clearer information on costs and fees associated with BNPL. |

| Debt Prevention | Restrictions on offering BNPL without robust affordability checks. |

In this shifting environment, UK banks must not only navigate the complexities of existing and future regulations but also reconsider their business strategies in relation to BNPL services. For institutions that actively embrace innovation while aligning with regulatory expectations, the future holds the potential for sustainable growth and consumer trust, making it imperative that they stay ahead of the curve in this dynamically changing financial ecosystem.

Regulatory Shifts: Key Changes on the Horizon for Buy Now Pay Later Services

Recent trends indicate that Buy Now Pay Later (BNPL) services are on the cusp of significant regulatory changes that could reshape the landscape for both consumers and providers. As these services gain popularity, regulators are increasingly scrutinizing their impact on financial health and consumer debts. Key changes anticipated in the near future include stricter affordability checks, enhanced disclosure requirements, and possible caps on fees charged to consumers. This shift aims not only to protect consumers but also to foster more responsible lending practices within the industry.

In response to these impending reforms, UK banks may find themselves reassessing their strategies and product offerings to align with new compliance standards. To remain competitive, banks might consider:

- Adopting advanced data analytics for better risk assessment

- Enhancing consumer education about BNPL terms and conditions

- Collaborating with fintech companies to integrate innovative payment solutions

Ultimately, the evolving regulatory environment presents both challenges and opportunities. As banks gear up for these changes, we may see a more transparent, sustainable ecosystem that prioritizes financial well-being for consumers, redefining the relationship between banks, regulators, and BNPL services.

Strategic Adaptations: How UK Banks Can Innovate in Response to BNPL Regulation

As UK banks face the rapid evolution of Buy Now Pay Later (BNPL) regulation, innovation will be key to adapting successfully. Embracing an agile strategy can allow banks to respond effectively to regulatory changes while enhancing customer experience. Potential strategic adaptations could include:

- Partnerships with fintechs: Collaborating with emerging financial technology companies can help banks leverage their innovative approaches and technology, providing customers with seamless payment options.

- Enhanced risk assessment models: Developing sophisticated algorithms that incorporate new data sources will enable banks to improve their credit decision-making processes and manage risk associated with BNPL products.

- Consumer education initiatives: Educating customers about responsible borrowing and the implications of BNPL, while offering tools for financial planning, can position banks as trusted advisors in personal finance management.

Moreover, re-invigorating product offerings in light of regulatory scrutiny will be essential. Consider the possibility of introducing transparent and flexible BNPL alternatives that foster responsible consumer behaviour. Some actionable ideas may include:

- Tailored repayment plans: Providing personalized payment schedules across various consumer demographics will enhance accessibility and satisfaction.

- Incorporating ethical lending practices: By limiting fees and offering fair interest rates, banks can demonstrate their commitment to ethical banking while adhering to new regulations.

- Utilizing data analytics: Leveraging data insights to predict customer behaviour and enhance product offerings will ensure banks remain competitive in the evolving financial landscape.

Future Outlook: Building a Sustainable Framework for Responsible Lending Practices

As the landscape of financial services continues to evolve, the emphasis on sustainability and responsibility in lending practices becomes paramount. UK banks must embrace a comprehensive framework that prioritizes ethical decision-making and consumer protection. This involves integrating advanced data analytics to assess individual borrower profiles more accurately and implementing robust creditworthiness assessments. Engaging with innovative technologies can help institutions to not only streamline processes but also enhance transparency and accountability in lending decisions.

Moreover, fostering collaboration between financial entities, regulators, and consumer organizations can create a more cohesive approach to responsible lending. A few key strategies could include:

- Education and Outreach: Providing clear and understandable information to consumers regarding their rights and responsibilities.

- Proactive Risk Management: Utilizing predictive analytics to identify potential borrower issues before they escalate.

- Ethical Product Development: Designing financial products that align with consumers’ best interests while facilitating responsible borrowing.

This collective effort will not only ensure compliance with upcoming regulatory demands but also pave the way for a sustainable financial ecosystem that prioritizes the needs of consumers and the well-being of the market.

To Conclude

In a landscape marked by rapid innovation and shifting consumer expectations, the future of Buy Now, Pay Later (BNPL) services in the UK stands at a crossroads. As regulators tighten their grip and banks adapt to evolving market dynamics, financial institutions must not only respond to these changes but embrace them as opportunities for growth and resilience.

Navigating this new terrain will require a delicate balance between fostering consumer access and ensuring responsible lending practices. The coming years will undoubtedly test the agility of UK banks as they align their strategies with regulatory frameworks designed to protect consumers while encouraging market innovation.

As we close this chapter on BNPL regulation and its implications, it becomes clear that the decisions made today will shape the financial landscape of tomorrow. With vigilance and adaptability, UK banks have the potential to redefine their roles, creating a future where both consumer interests and institutional integrity thrive. The road ahead is complex, but with foresight and collaboration, the journey promises to be transformative.