In an era where financial systems around the globe are increasingly being asked to adapt to the demands of a digital-first economy, Brazil stands out as a beacon of innovation with its remarkable open banking framework. Launched in 2021 as part of a sweeping reform, Brazil’s open banking initiative has not only transformed the country’s financial landscape but has also sparked conversations about its potential as a model for other nations. With its emphasis on transparency, competition, and enhanced consumer choice, Brazil’s approach offers a compelling case study for the United States, where the push for a similar system is gaining momentum. This article delves into the key components of Brazil’s open banking success, explores the benefits and challenges it presents, and examines how its lessons could pave the way for a more inclusive and dynamic financial ecosystem in the US. As we analyse this evolving narrative, the question lingers: Could Brazil’s innovative blueprint be the catalyst for a new era in American banking?

Brazil’s Open Banking Journey: Key Milestones and Innovations

Brazil’s journey into open banking has been marked by a series of key milestones that have revolutionized the financial landscape. Starting in 2018, the Central Bank of Brazil established the framework for open banking, aimed at increasing competition and enhancing consumer experience. Some of the most significant developments include:

- Implementation of Regulatory Framework: The formal adoption of rules in December 2020 set the stage for banks and fintechs to share customer data.

- Launch of Phases: The gradual rollout divided into four phases allowed for structured implementation and feedback loops.

- Increased Participation: Thousands of institutions, including banks, fintechs, and third-party providers, embraced open banking, fostering innovation.

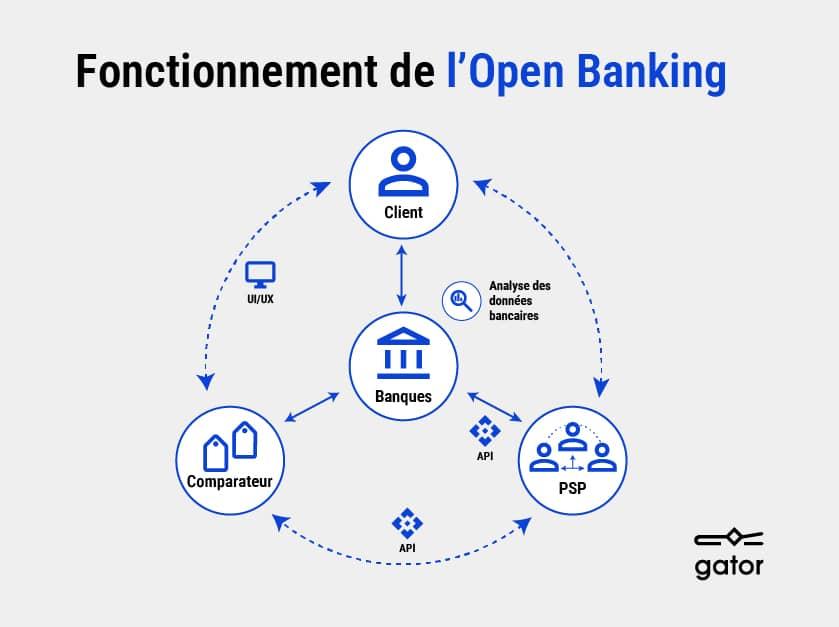

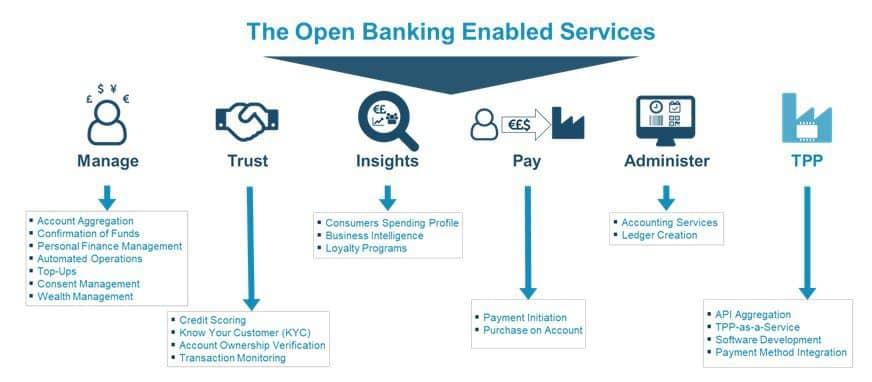

Innovations in Brazil’s open banking ecosystem have emerged from this collaborative atmosphere. Notably, the integration of APIs (Application Programming Interfaces) has enabled seamless data sharing, empowering consumers to manage their financial activities better. Here’s a breakdown of some transformative innovations:

| Innovation | Description |

|---|---|

| Data Aggregation | Consumers can access diverse financial accounts through one platform, enhancing visibility and control. |

| Personalized Financial Products | Fintechs leverage data to tailor financial solutions that meet individual consumer needs. |

| Cross-Border Services | New partnerships enable users to access international financial services, expanding market reach. |

Building Consumer Trust: Transparency and Security in Open Banking

In the fast-evolving landscape of open banking, establishing consumer trust hinges significantly on two critical pillars: transparency and security. Brazilian open banking initiatives have laid the groundwork for a robust framework that fosters confidence among users. Consumers now expect to understand how their financial data is managed, accessed, and utilized, leading to a demand for clear and straightforward policies. By openly sharing information regarding data usage, financial institutions can empower consumers with the knowledge they need to make educated decisions. This transparency not only enhances customer satisfaction but also cultivates long-lasting relationships based on mutual respect and understanding.

To bolster these efforts, security measures play an equally vital role in reinforcing trust. In Brazil, the implementation of advanced encryption technologies and rigorous access controls has been paramount in safeguarding sensitive financial information. By adopting a multi-layered security approach, institutions can reassure consumers that their data is not just managed with integrity but is also protected from potential threats. Key components of this security model include:

- Robust encryption protocols

- Regular security audits

- Incident response strategies

Together, transparency and security form a symbiotic relationship that not only enhances the open banking experience but also sets a precedent for the U.S. market. As consumers become increasingly aware of their rights regarding financial data ownership, these principles are essential for any country aiming to replicate Brazil’s success in open banking.

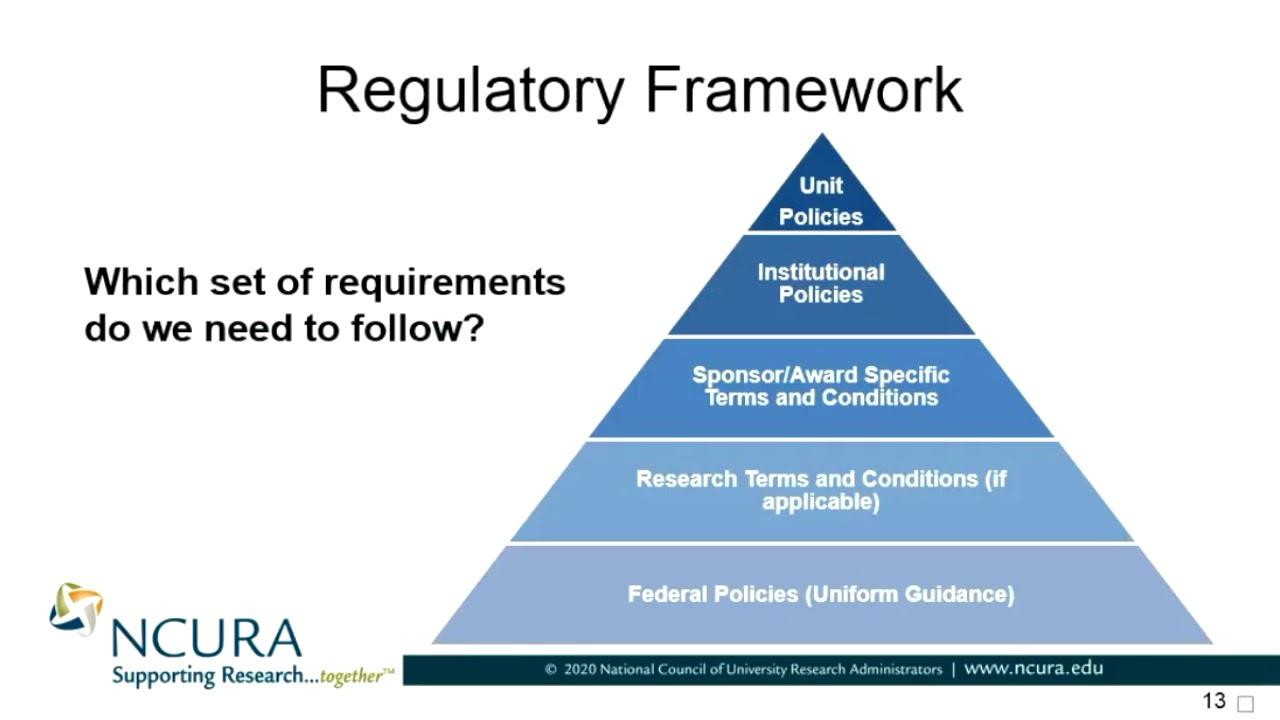

Regulatory Frameworks: Lessons from Brazil for the US Market

Brazil’s approach to open banking offers a compelling case study for the United States, highlighting key regulatory frameworks that facilitated a seamless transition into a more competitive banking ecosystem. The Brazilian government instituted a phased implementation strategy, which allowed financial institutions to gradually adapt to new regulations without overwhelming their operational capacities. This strategy included clear timelines, well-defined roles for regulatory bodies, and collaborative workshops involving banks and fintech firms. The result has been not only increased financial inclusion but also enhanced customer services, thanks to a diverse array of products and services emerging from this competitive landscape.

In addition, the Brazilian experience underscores the importance of consumer trust and security in instilling confidence in open banking. Robust data protection regulations were essential to mitigate concerns over privacy and unauthorized data sharing. Key lessons include the need for transparency in data usage, comprehensive consumer education, and mechanisms for grievance redressal. To create an effective framework in the US, policymakers might consider implementing:

- Clear guidelines on consent and data ownership

- Collaboration between traditional banks and emerging fintech players

- Continuous engagement with stakeholders through public consultations

Fostering Collaboration: How Partnerships Can Drive Open Banking Success

In the rapidly evolving landscape of open banking, partnerships are becoming the cornerstone of success. By fostering collaboration across financial institutions, technology providers, and regulatory bodies, stakeholders can unlock innovative solutions that enhance user experience and drive market growth. Key players in the financial sector are recognizing that leveraging their strengths through alliances can lead to valuable propositions, such as improved digital services, lower consumer costs, and increased access to financial products. The Brazilian open banking model demonstrates that a collaborative approach not only facilitates compliance with regulatory requirements but also stimulates competition, ultimately benefiting the consumer.

To cultivate an environment conducive to success, it’s essential to establish clear frameworks for cooperation. Here are a few fundamental elements that can drive these partnerships:

- Shared Goals: Align objectives among all partners to ensure a unified vision.

- Open Communication: Foster transparency to build trust and facilitate problem-solving.

- Resource Pooling: Combine strengths and assets to create synergistic advantages.

- Regulatory Compliance: Work closely with regulators to navigate the complexities of the open banking landscape.

A tangible example of successful collaboration can be illustrated in the table below, showcasing three Brazilian fintechs that partnered with traditional banks:

| Fintech Partner | Bank Partner | Collaboration Highlights |

|---|---|---|

| Banco Inter | BTG Pactual | Joint platforms for investment products |

| Nubank | Caixa Econômica Federal | Expanded payment options for consumers |

| PicPay | Banco do Brasil | Facilitated instant transactions |

These partnerships not only innovate solutions but also significantly enhance customer engagement, setting a formidable precedent for other regions contemplating the implementation of open banking initiatives.

Closing Remarks

As we conclude our exploration of Brazil’s remarkable journey into the realm of open banking, it becomes evident that this dynamic framework has not only transformed the financial landscape of a nation but also carved a path ripe with lessons for others to follow, including the United States. Brazil’s innovative approach showcases the potential for enhanced consumer choice, increased competition, and streamlined financial services that have, in many ways, redefined the banking experience.

While the U.S. grapples with its own regulatory nuances and market challenges, the Brazilian model serves as both inspiration and cautionary tale. By examining these successes and pitfalls, American policymakers and financial institutions have a prime opportunity to tailor a more inclusive, efficient, and customer-centric banking environment.

The question remains: will the U.S. seize this moment to embrace a similar transformation? As the financial sectors across the globe evolve, one thing is clear: the possibilities borne from Brazil’s open banking revolution could very well ignite a new era of innovation and accessibility for consumers everywhere. The future of finance awaits; it is up to us to chart the course.