Navigating Tomorrow: Key Disruptions in Lending Practices

In an age where technological advancements and shifting consumer behaviors are transforming industries at an unprecedented pace, the financial sector stands at a crossroads. Traditional lending practices, once anchored in established protocols and face-to-face interactions, are increasingly being redefined by innovation and disruption. From the rise of fintech solutions to the integration of artificial intelligence and blockchain, the landscape of lending is evolving, presenting both challenges and opportunities for borrowers and lenders alike. As we delve into the key disruptions shaping the future of lending, we invite you to explore how these changes are not only redefining access to capital but also reshaping the very fabric of financial relationships. Join us on a journey to understand the pathways of tomorrow’s lending practices, where adaptability and foresight are essential for navigating a rapidly changing environment.

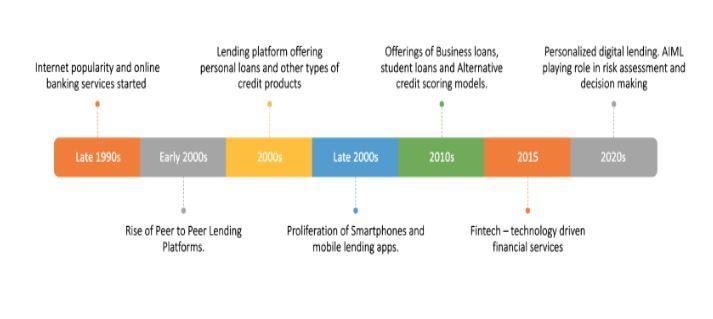

Understanding the Evolution of Lending in a Digital Landscape

The transformation of lending practices has been profound, particularly with the advent of technology that has reshaped consumer expectations and financial institutions’ capabilities. Traditionally dominated by banks, the lending landscape is now characterized by a diverse array of digital platforms that prioritize customer experience. Peer-to-peer lending, microfinancing, and crowdfunding have provided borrowers with alternative avenues to access funds, often bypassing the conventional barriers imposed by traditional banks. This evolution fosters increased competition, driving interest rates down and making borrowing more accessible to a broader audience.

Moreover, the integration of advanced technologies such as artificial intelligence and machine learning is revolutionizing how lending decisions are made. These innovations enable lenders to analyze vast datasets quickly, assessing creditworthiness more accurately and reducing the risk of defaults. Key attributes of this technological shift include:

- Enhanced Credit Scoring: Utilizing alternative data sources for a more comprehensive view of a borrower’s credit risk.

- Real-Time Decision Making: Streamlined processes that allow for instant approvals and fund disbursement.

- Personalized Lending Solutions: Tailored loan products developed using insights from user behavior and preferences.

With this shift, lending practices are not just evolving but dynamically adapting to meet the needs of today’s consumers, setting the stage for future innovations in finance.

Embracing Technological Innovations to Enhance Customer Experience

In an era defined by rapid technological advancement, the lending industry stands on the cusp of transformation, with innovative tools reshaping how institutions interact with their customers. By leveraging data analytics, artificial intelligence, and machine learning, lenders can create highly personalized experiences that cater to individual needs. This is particularly evident in the adoption of chatbots and virtual assistants, enabling customers to receive instant responses to their inquiries. Moreover, the incorporation of blockchain technology ensures secure transactions and transparent processes, which fosters trust and enhances customer satisfaction.

The integration of technology also paves the way for streamlined application processes and quicker approvals. Lenders are increasingly utilizing digital platforms to reduce paperwork and eliminate unnecessary delays. The benefits can be summarized as follows:

- Instantaneous Approval: Automated systems can evaluate applications in real-time.

- Enhanced Accessibility: Customers can access services anytime, anywhere, via mobile apps.

- Personalized Offers: Analysis of consumer behavior allows lenders to tailor products based on unique profiles.

This proactive embrace of technology not only improves operational efficiency but also cultivates a deeper relationship with customers, who are empowered with the convenience, speed, and transparency they increasingly demand.

| Innovation | Impact on Customer Experience |

|---|---|

| Data Analytics | Customized service offerings |

| AI Chatbots | 24/7 customer support |

| Blockchain | Increased security and trust |

| Digital Platforms | Quick and easy applications |

Mitigating Risks in a Data-Driven World

In a landscape characterized by rapid technological advancements and shifting consumer expectations, financial institutions must adopt a proactive approach to risk management. Data governance emerges as a critical component, ensuring that data used for decision-making is accurate, comprehensive, and secure. By implementing robust systems that regularly audit data integrity, lenders can minimize exposure to fraud and enhance compliance with regulatory requirements. Additionally, investing in advanced analytics allows for deeper insights into borrower behavior, enabling companies to identify emerging risks before they escalate into significant issues.

Furthermore, leveraging machine learning algorithms can provide real-time assessment of creditworthiness, helping to mitigate risks associated with default. This technological shift not only enhances predictive accuracy but also supports a more personalized lending experience for consumers. Institutions must also prioritize cybersecurity measures, as the rise in digital transactions opens new avenues for data breaches. A strategic approach to risk management should incorporate:

- Regular Training: Equip employees with the knowledge to identify and combat cyber threats.

- Incident Response Plans: Develop and practice protocols for addressing potential breaches swiftly.

- Collaborative Partnerships: Work with fintech companies to share data science insights and strengthen defenses.

Strategic Adaptations for Future-Ready Lending Practices

The lending landscape is undergoing significant transformations, necessitating a shift in strategies that ensure organizations remain competitive and responsive to evolving borrower needs. Data-driven decision-making is at the forefront of these advancements, allowing lenders to leverage insights gathered from customer behavior, credit history, and market trends. By harnessing artificial intelligence and machine learning, institutions can enhance risk assessment processes, streamline applications, and tailor products to suit diverse client profiles. Embracing technology not only improves operational efficiency but also fosters a more personalized lending experience that meets the demands of the digital age.

To build a future-ready lending framework, organizations must focus on several key areas:

- Customer Engagement: Implementing omnichannel communication strategies to connect with borrowers at various touchpoints.

- Regulatory Compliance: Staying ahead of changing regulations and ensuring transparent practices that instill confidence in customers.

- Partnerships: Collaborating with fintech companies to innovate product offerings and reach broader demographics.

- Sustainability Initiatives: Integrating environmentally sustainable practices into lending processes to attract socially-conscious borrowers.

Furthermore, a strategic focus on financial literacy programs can empower borrowers, improving their understanding of credit, loan structures, and responsible borrowing practices. This educational approach is not only beneficial for the customer but also reduces default rates, fostering a healthier lending ecosystem. By prioritizing these comprehensive adaptations, organizations will position themselves as leaders in the industry, ready to navigate the challenges that lie ahead.

Concluding Remarks

As we stand on the precipice of a new era in lending, it is essential to recognize that the changes we are witnessing today are not mere trends but rather a fundamental reshaping of the financial landscape. The rise of technology, shifting consumer expectations, and evolving regulatory frameworks are all set to define the way we borrow and lend in the years to come.

In navigating these disruptions, stakeholders—from traditional banks to fintech innovators—must embrace agility and adaptability, anticipating the needs of a more informed and empowered clientele. As we look towards tomorrow, the key will be not just to respond to these changes, but to proactively shape the future of lending practices.

The journey ahead is filled with both challenges and opportunities. By fostering a culture of collaboration and innovation, we can create a lending ecosystem that is not only efficient and accessible but also inclusive and responsible. The discussions we’ve initiated today will be critical as we forge a path forward, ensuring that the evolution of lending benefits all participants in the financial realm. As we close this chapter, let us remain vigilant and open-minded, ready to embrace the possibilities that await in the ever-changing world of finance.