Navigating Change: BNPL Regulation’s Ripple Effect on UK Banks

In the fast-paced landscape of consumer finance, few developments have captured the public’s attention quite like Buy Now, Pay Later (BNPL) schemes. These innovative payment solutions have blurred the lines between immediate gratification and financial responsibility, offering consumers unprecedented flexibility. However, as the popularity of BNPL surges, so too does scrutiny from regulators eager to ensure consumer protection and market stability. In the UK, the recent wave of regulation aimed at BNPL providers is set to create ripples that extend far beyond the point of sale. This article delves into the multifaceted implications of these regulatory shifts on UK banks, exploring how the evolving landscape of BNPL is reshaping traditional banking practices and prompting financial institutions to adapt in order to remain competitive in an ever-changing market. Join us as we navigate the currents of change and uncover what lies ahead for both consumers and banks in this transformative era.

Understanding the Landscape of BNPL Regulation and Its Impact on Banking Practices

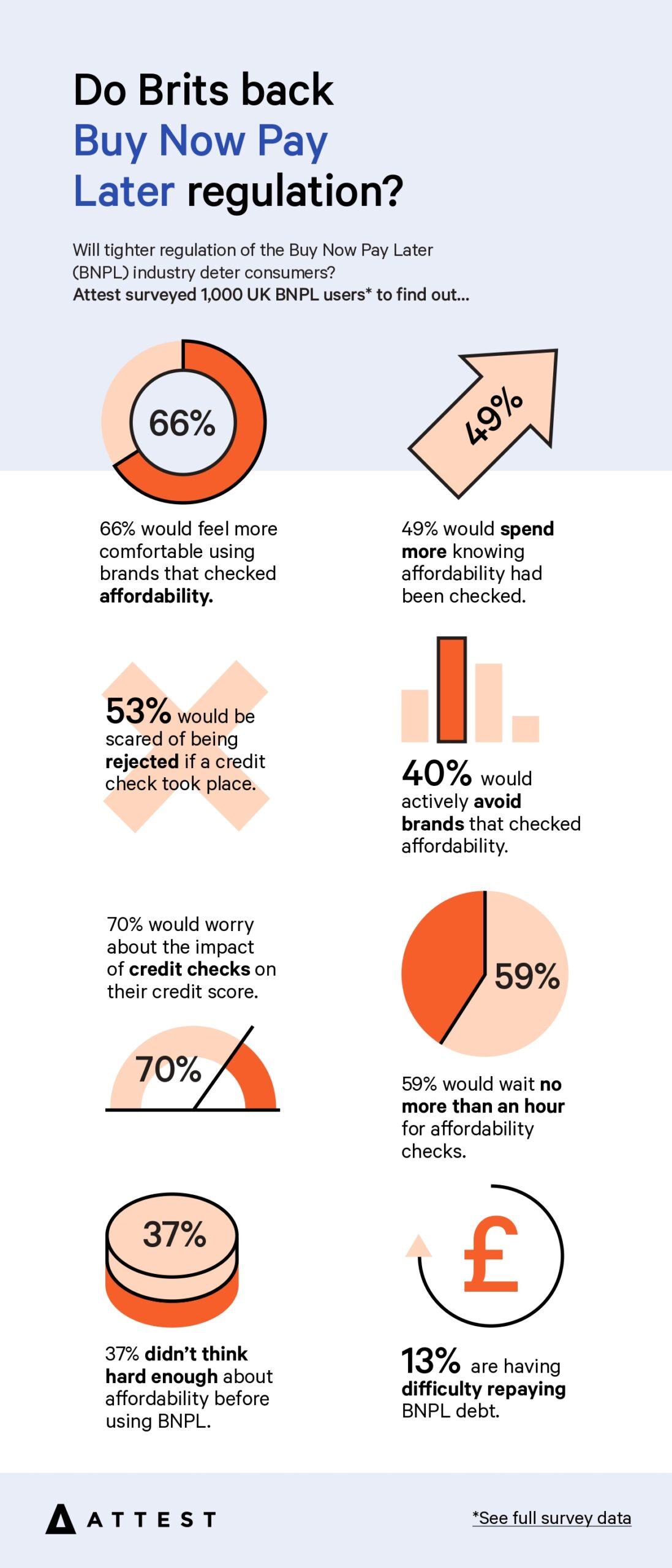

The rise of Buy Now Pay Later (BNPL) schemes has significantly transformed consumer financing, prompting regulators to take a closer look at their implications. In the UK, this regulatory scrutiny is leading to a more structured framework designed to protect consumers while ensuring fair competition in the banking sector. As these regulations evolve, financial institutions must adapt their practices to navigate the newly established landscape. Key elements of the regulation include:

- Mandatory Affordability Checks: Banks will need to implement stringent assessments to ensure that consumers can meet their repayments.

- Transparent Cost Disclosures: Institutions must clearly inform customers about fees and potential penalties associated with BNPL services.

- Consumer Protection Measures: Enhanced safeguards will be put in place to minimize risks of over-indebtedness among consumers.

As banks reassess their roles in an increasingly competitive market influenced by alternative lenders, compliance with BNPL regulations poses both challenges and opportunities. Financial institutions may need to re-evaluate their product offerings and ensure they remain attractive yet compliant. This regulatory framework is likely to encourage collaboration between traditional banks and fintech companies, creating an ecosystem where innovation can flourish within safe boundaries. A potential outcome of these changes can be illustrated in the following table:

| Impact | Banking Practices |

|---|---|

| Increased Compliance Costs | Enhanced risk management protocols |

| Heightened Consumer Awareness | Focus on financial literacy programs |

| Shifts in Customer Preferences | Adaptation of service models to meet demand |

Assessing the Financial Health of UK Banks Amidst Regulatory Transformations

The recent waves of regulatory changes affecting the Buy Now, Pay Later (BNPL) landscape are compelling UK banks to reassess their financial health and strategic positioning. As the Financial Conduct Authority (FCA) tightens oversight, banks face new compliance costs and operational challenges. They must now focus on enhancing their risk management frameworks to mitigate exposure to unsecured lending, which has become increasingly prominent with the rise of BNPL options. Key considerations include:

- Credit Risk Assessment: Banks need to revisit their credit scoring models to adapt to the evolving consumer behavior associated with BNPL products.

- Liquidity Management: Regulatory changes may pressure liquidity ratios as banks balance short-term lending with customer repayments.

- Capital Reserves: To absorb potential losses, banks must evaluate the adequacy of their capital reserves in light of new lending risks.

In this shifting landscape, the financial performance of UK banks will largely depend on their ability to innovate while managing these new regulatory challenges. The introduction of compliance requirements may also lead to a reshuffle in market dynamics, influencing how banks interact with technology firms that dominate the BNPL sector. A comparative analysis reveals the need for strategic alignment between traditional banking practices and agile fintech solutions:

| Institution Type | Current BNPL Exposure | Regulatory Compliance Status |

|---|---|---|

| Traditional Banks | Moderate | Undergoing adjustments |

| Fintech Companies | High | Adopting new standards |

| Hybrid Models | Variable | Implementing proactive measures |

Strategies for UK Banks to Adapt and Thrive in a Changing BNPL Environment

As UK banks grapple with the evolving landscape of Buy Now Pay Later (BNPL) services, it is crucial for them to assess new regulatory frameworks and consumer trends to remain competitive. First, banks should enhance their partnerships with fintech companies to leverage innovative technologies and capture the market share that BNPL providers have gained. By incorporating digital payment products into their offerings, banks can create a seamless ecosystem that appeals to consumers who prefer flexible payment options. Second, investing in advanced data analytics can provide insights into customer behavior, allowing banks to develop tailored financial products that meet the specific needs of their clientele.

Moreover, agility in product offerings will be essential. Banks must consider optimizing their existing credit models and reevaluating risk assessment strategies to address the shift in consumer credit preferences. Key strategies include:

- Implementing responsible lending practices to ensure customer protection

- Creating attractive loyalty programs that rival BNPL incentives

- Educating consumers on financial literacy and the implications of using credit

To illustrate the potential benefits of these strategies, a simple framework can guide banks in their adaptation:

| Strategy | Benefit |

|---|---|

| Partnerships with Fintech | Access to innovative technology and wider market reach |

| Data Analytics Investment | Improved customer insights and tailored product offerings |

| Agile Credit Models | Enhanced risk management and competitive positioning |

Future-Proofing Banking Operations: Recommendations for Embracing Regulatory Change

As the UK banking sector navigates the evolving landscape of regulations, particularly with the advent of Buy Now, Pay Later (BNPL) schemes, it becomes crucial for institutions to adapt proactively. Banks must not only comply with current regulations but also anticipate future changes that can significantly impact operations. Engaging a multi-disciplinary approach by integrating legal, compliance, and fintech experts can bolster banks’ ability to respond effectively. Areas to focus on include:

- Enhanced Data Analytics: Utilizing advanced data analytics tools to monitor compliance in real-time.

- Cross-Functional Training: Ensuring staff across departments understand regulatory requirements and the implications of BNPL offerings.

- Consumer Education Programs: Offering resources to inform customers about responsible borrowing practices.

Moreover, investing in technology and innovation is paramount in safeguarding against regulatory pitfalls. To illustrate a roadmap for progress, banks can consider implementing the following strategies:

| Strategy | Description |

|---|---|

| RegTech Solutions | Implementing regulatory technology to streamline compliance processes. |

| Collaboration with Regulators | Establishing ongoing dialogues with regulatory bodies to stay ahead of changes. |

| Agile Framework Adoption | Adopting an agile project management methodology to enhance adaptability. |

Insights and Conclusions

As we traverse the evolving landscape of Buy Now, Pay Later (BNPL) regulation, it becomes clear that the ripples of change are felt far beyond the confines of individual transactions. For UK banks, the advent of stricter guidelines presents both a challenge and an opportunity—a chance to innovate and reimagine their role in a marketplace that increasingly values transparency and consumer protection.

In this era of transformation, the path forward is fraught with complexities, compelling financial institutions to rethink strategies and adapt to a new regulatory climate. Yet, amidst the uncertainty, there lies a silver lining: the potential for enhanced customer trust, a more stable financial ecosystem, and the nurturing of responsible lending practices.

As we step into this next chapter, staying attuned to the regulatory winds will be crucial for banks aiming not just to survive, but to thrive in a world where consumers demand clarity and security. The journey may be challenging, but it also holds the promise of reshaping the financial landscape for the better—one regulation at a time.