In an era marked by rapid technological advancements and an ever-evolving financial landscape, the European Union is stepping forward with a transformative initiative poised to reshape the way we think about payments. Enter the Payment Services Directive 3 (PSD3), a groundbreaking legislative framework designed to enhance the resilience, security, and efficiency of payment systems across Europe. As digital transactions become increasingly ingrained in our daily lives, PSD3 serves not only as a regulatory response to the challenges of a complex digital economy but also as a blueprint for fostering innovation and competition in the payments sector. This article delves into the pivotal features of PSD3, its implications for consumers and businesses alike, and the potential it holds for forging a more robust and inclusive payments future within the EU and beyond. Join us as we explore the intricacies of this landmark directive and its promise to redefine the financial playing field.

Understanding the Core Principles of PSD3 and Their Impact on Payment Systems

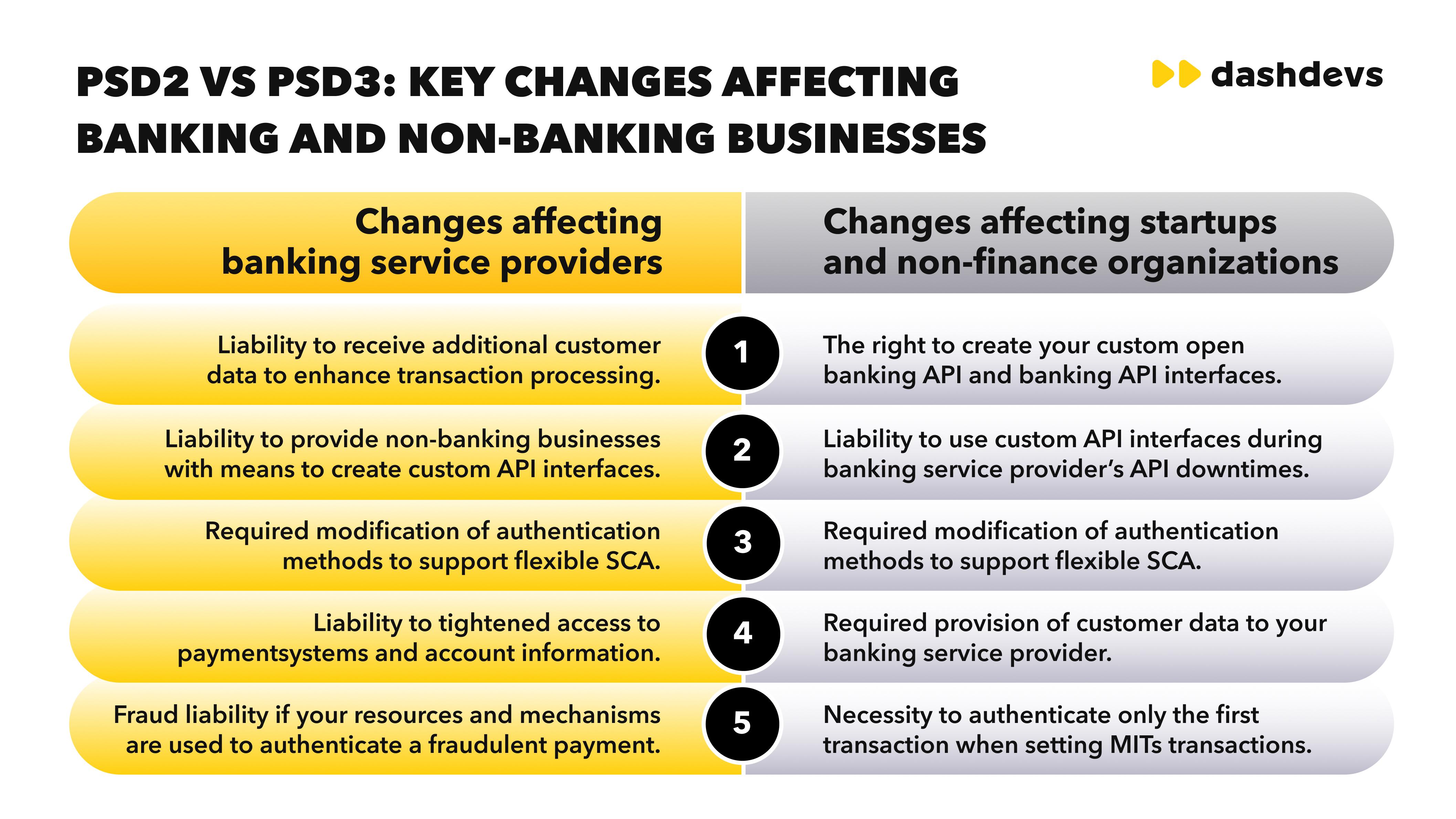

The third iteration of the Payment Services Directive, or PSD3, is poised to reshape the regulatory landscape of payment services across the European Union. With the rapid evolution of digital transactions, PSD3 seeks to fortify the financial ecosystem by introducing core principles that focus on enhanced security, innovation, and consumer protection. Key elements include strong customer authentication, which demands additional verification layers, as well as the promotion of open banking, thereby enabling third-party providers to integrate seamlessly with existing banking infrastructures.

Moreover, PSD3 emphasizes the importance of interoperability and transparency within the payment systems. This is set to offer consumers a wider range of options while fostering competition among service providers. Notably, these principles will facilitate a shift towards more sustainable payment methods, aligning with the EU’s broader sustainability goals. As the directive unfolds, its implementation is anticipated to bring forth a more resilient and consumer-friendly payment landscape through:

- Improved Security Measures: Enhanced protections against fraud and data breaches.

- Increased Transparency: Clearer fee structures and service conditions for consumers.

- Fostering Innovation: Encouraging fintech solutions to enhance user experiences.

Navigating Enhanced Security Features in PSD3 for Safer Transactions

As the Payment Services Directive 3 (PSD3) takes shape, users and businesses alike must adapt to its enriched security protocols aimed at fortifying digital transactions. A prime focus of PSD3 is to enhance strong customer authentication (SCA), ensuring that both sides of a transaction are safeguarded against potential cyber threats. This regime introduces new layers of verification that may include biometric factors, such as fingerprint scanning or facial recognition, alongside traditional methods like passwords and PINs. Moreover, the directive mandates the use of dynamic linking, whereby transaction details must be authenticated in real-time, reducing the likelihood of fraud by creating unique transaction signatures.

To further bolster security, PSD3 emphasizes transaction monitoring and risk assessment procedures for payment service providers. This involves employing advanced algorithms and machine learning technologies to analyze patterns and identify anomalies during transactions. By evaluating risk in real-time, service providers can quickly flag suspicious activities and mitigate potential breaches. The directive also outlines guidelines for better customer information management, ensuring that sensitive data remains protected through encryption and secure storage methodologies. The proactive steps laid out in PSD3 aim not only to protect consumers but also to instill confidence in the overall payment ecosystem.

Empowering Consumers through Transparency and Choice in the Payment Landscape

In an era where consumers demand greater control over their financial decisions, the European Union’s PSD3 aims to create a more transparent payments environment. By prioritizing consumer rights and data protection, PSD3 encourages payment providers to disclose essential information, allowing users to make informed choices. This level of transparency not only fosters trust between consumers and service providers but also promotes competition within the payments market. As a result, consumers are empowered to select payment options that best suit their needs, be it in terms of fees, speed, or security.

Furthermore, one of the standout features of PSD3 is its emphasis on open banking and interoperability among payment platforms. This innovation enables various financial services to seamlessly connect, providing consumers with enhanced flexibility. The introduction of standardized APIs means that users can easily switch between different payment methods without facing compatibility issues. A clear understanding of the benefits can be illustrated as follows:

| Feature | Benefit for Consumers |

|---|---|

| Transparency | Informed choices based on clear pricing structures |

| Open Banking | Seamless access to multiple financial services |

| Interoperability | Flexibility to switch payment methods without hassle |

This framework is set to revolutionize the payment landscape, placing power firmly in the hands of the consumer. With these advancements, the future of payments not only looks resilient but also increasingly consumer-centric, encouraging a dynamic environment where users can thrive.

Recommendations for Stakeholders to Prepare for the PSD3 Transition

As we embark on the transition to PSD3, it’s crucial for stakeholders—including financial institutions, payment service providers, and regulatory bodies—to take proactive measures. Risk assessment should be at the forefront of all strategies, tackling vulnerabilities that may arise from the new regulations. Implementing a robust compliance framework is essential to navigate the complex landscape of PSD3 while minimizing disruptions. Engage in collaborative workshops with industry peers to share insights and develop best practices, fostering a community of knowledge that strengthens the entire ecosystem.

Additionally, stakeholders should prioritize technology upgrades to meet new compatibility standards outlined in PSD3. Investing in open banking solutions will not only enhance customer experience but also align with the regulatory push towards greater financial transparency. Consider leveraging data analytics to gain insights into consumer behavior, which can inform product offerings tailored to evolving market needs. Building a flexible and responsive customer support system will facilitate smooth transitions and help address any concerns arising from regulatory changes.

The Conclusion

As we conclude our exploration of PSD3 and its implications for the future of payments within the European Union, it becomes evident that this regulatory framework is more than just a set of guidelines; it is a visionary blueprint designed to foster resilience, security, and inclusivity in the financial landscape. By embracing innovation while ensuring robust consumer protection, PSD3 aims to empower both businesses and consumers in an increasingly digital economy.

As we stand on the brink of a new era in payment systems, the potential for enhanced interoperability and streamlined processes heralds a future where transactions are not only faster and safer but also more accessible. The success of PSD3 will depend on its implementation and the collaborative efforts of industry stakeholders, regulators, and consumers alike.

In this dynamic landscape, the path may be fraught with challenges, but the promise of a secure and innovative payment ecosystem is a horizon worth pursuing. Let us keep a watchful eye on PSD3 as it unfolds, for it holds the key to shaping the next chapter in Europe’s financial narrative—a chapter brimming with possibilities, where resilience meets innovation on the path to a truly interconnected payments future.