In an era where digital transformation is reshaping industries, the banking sector stands at a pivotal crossroads, grappling with the challenge of modernization while striving to retain customer trust and operational efficiency. As financial institutions evolve to meet the demands of a tech-savvy clientele, the concept of interoperability emerges as a crucial lifeline—a bridge connecting disparate systems, enhancing communication, and fostering innovation. “Bridging the Gap: Interoperability in Bank Modernization” delves into the intricacies of this essential undertaking, exploring how banks can harmonize legacy infrastructures with contemporary technologies. From enhancing customer experiences to streamlining internal processes, this article will illuminate the pathways to a future where seamless interaction is not just a possibility, but a foundational principle of our banking systems. Join us as we navigate the challenges and opportunities that lie ahead in the quest for a more interconnected financial world.

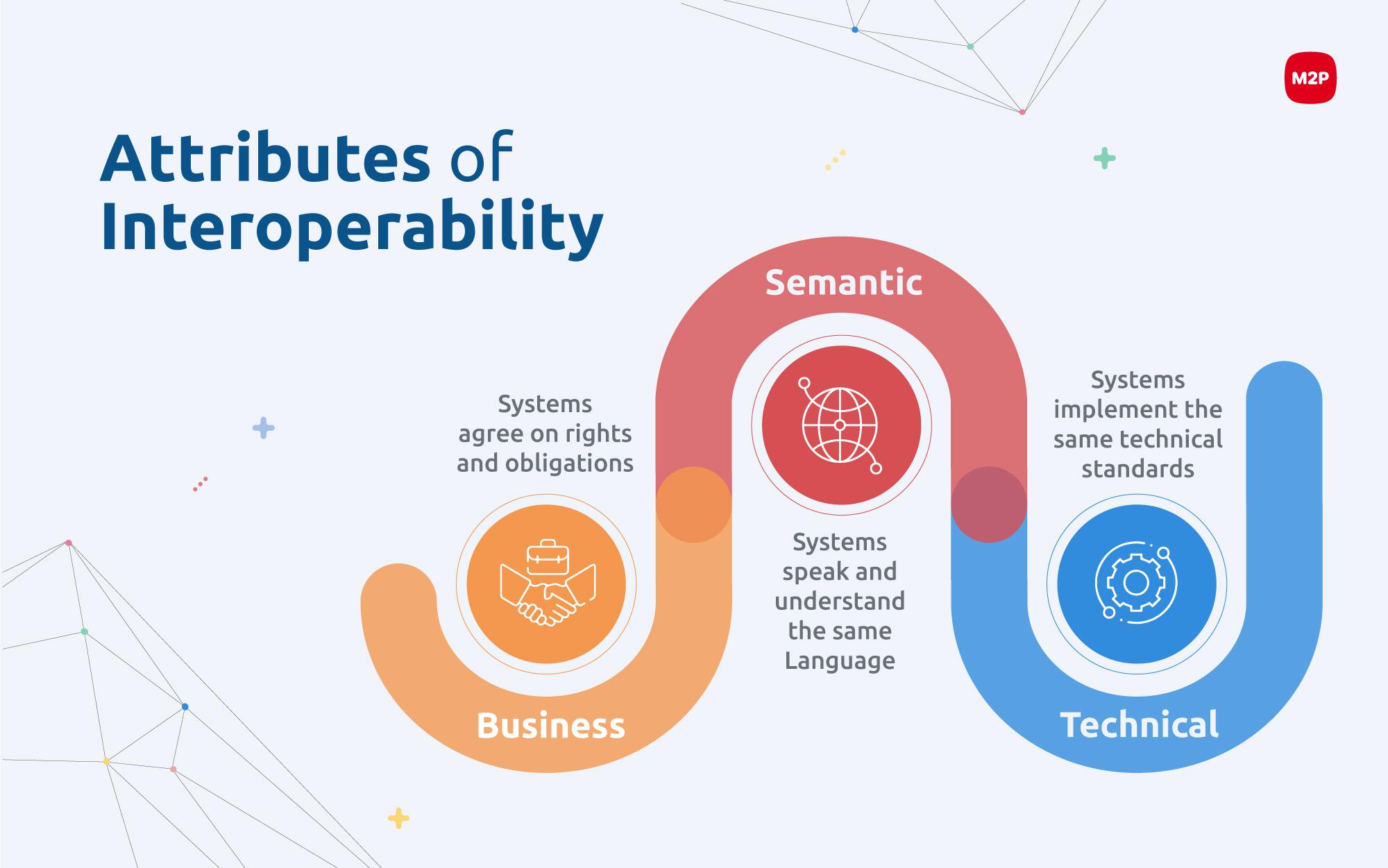

Understanding Interoperabilitys Role in Modern Banking

The financial landscape is rapidly evolving, driven by customer demand for seamless experiences and the influx of emerging technologies. In this context, interoperability emerges as a vital component for modern banks striving to remain competitive. By allowing different systems to communicate effectively, it enables a more fluid exchange of information across various platforms and institutions. This interconnectedness not only minimizes discrepancies and data silos but also enhances operational efficiency, ensuring financial institutions can adapt to changing regulations and customer expectations swiftly.

Furthermore, the significance of interoperability extends to fostering innovation within the banking sector. As new fintech solutions and digital services proliferate, a robust interoperable framework allows for the integration of diverse products and services, thereby enriching the customer experience. Banks can develop collaborative ecosystems with third-party developers and other financial institutions, leading to offerings that are more versatile. The benefits of embracing this paradigm shift in technology can be summarized as follows:

- Enhanced Customer Experience: Seamless transactions and faster service delivery.

- Increased Flexibility: Ability to integrate with various technologies and adapt to market changes.

- Cost Efficiency: Reduction in operational costs through streamlined processes.

Key Challenges in Achieving Seamless Integration

In the rapidly evolving landscape of digital banking, achieving seamless integration between legacy systems and modern technologies presents a host of challenges. Data silos are often one of the primary obstacles, as older systems were not designed to communicate effectively with newer applications. This creates an environment where critical information is trapped within disparate systems, leading to inefficiencies and increased operational costs. Moreover, the complexity of regulatory compliance adds another layer of difficulty, as different regions and jurisdictions have varying requirements. Organizations must navigate these regulations while ensuring data integrity and security throughout the integration process.

Another significant hurdle is the cultural resistance to change within financial institutions. Employees accustomed to traditional workflows may find it challenging to adapt to new technologies and processes. This can result in a reluctance to embrace new solutions, hampering the modernization efforts. Additionally, the fast pace of technological advancements means that institutions constantly need to update and retrain their personnel. Financial institutions must also contend with the interoperability of multiple platforms, which can complicate the integration process further. Each system may have its own architecture and standards, making it difficult to create a cohesive ecosystem that enhances user experience and operational efficiency.

Best Practices for Implementing Interoperable Solutions

To successfully implement interoperable solutions in bank modernization, institutions should prioritize collaboration among stakeholders. Engaging all parties—from IT teams to customer service representatives—ensures that everyone’s insights contribute to a cohesive strategy. Regular workshops and brainstorming sessions can foster a culture of innovation and alignment. Additionally, organizations must develop a clear framework for integration by establishing guidelines that promote standardization across platforms. This harmonization not only streamlines processes but also enhances the customer experience by providing seamless access to banking services.

Moreover, adopting a phased approach to implementation can mitigate risks while allowing for iterative improvements. Start by identifying core systems that require interoperability and gradually expand to more complex functionalities. Utilizing API-first design principles enables quicker adaptations to changing market trends, leading to a more agile banking environment. Regular assessments and feedback loops should be incorporated to refine the solutions continually. By focusing on these key areas, banks can create an adaptive infrastructure capable of accommodating future technological advancements, ensuring long-term sustainability and competitiveness.

Future Trends Shaping Interoperability in Financial Institutions

As financial institutions continue to modernize their operations, several trends are emerging that significantly impact interoperability. The rise of cloud computing is leading the charge, enabling banks to adopt scalable solutions that facilitate data sharing across different platforms securely. Additionally, the implementation of Application Programming Interfaces (APIs) is transforming the landscape, allowing banks to seamlessly connect and exchange information with various third-party providers. This development not only enhances customer experience through personalized services but also fosters innovation by enabling new financial products to be built on existing platforms.

Another crucial trend shaping interoperability is the advancement of blockchain technology, which offers a decentralized approach to transactions while ensuring transparency and security. By leveraging smart contracts, banks can automate processes and reduce discrepancies that often arise during data exchanges. Furthermore, the growing emphasis on regulatory compliance is pushing institutions to adopt standardized protocols that simplify inter-organizational communication. This standardization is crucial, as it mitigates risks related to data breaches and streamlines reporting processes across different jurisdictions.

Insights and Conclusions

As we navigate the intricate landscape of bank modernization, the quest for interoperability emerges as a critical beacon guiding financial institutions toward a more integrated and efficient future. The convergence of legacy systems with innovative technologies is not merely a technical challenge; it is a fundamental shift aimed at enhancing the customer experience, improving operational efficiencies, and ultimately driving growth.

In bridging the gap between past and present, banks are not only reimagining their internal frameworks, but they are also fostering a collaborative ecosystem that promotes innovation and responsiveness in a rapidly evolving market. As stakeholders—from technology providers to regulators—come together, the prospects for a cohesive banking environment grow ever brighter.

While the path may be fraught with obstacles, the continuous dialog surrounding interoperability lays the groundwork for solutions that can accommodate diverse needs. In this ever-changing digital realm, the ability to communicate seamlessly within and across platforms will be the linchpin for success.

As we look toward the horizon, the journey toward a fully interoperable banking landscape reminds us that in the world of finance, unity breeds strength. It is not just about modernization; it’s about creating a robust future where every transaction is effortless, every experience is enriched, and every participant can thrive. The call to action is clear: let us embrace the collaborative spirit needed to bridge these gaps, ensuring a better banking experience for all.