In an era defined by rapid technological advancement and shifting regulatory landscapes, the financial sector stands at a pivotal crossroads. Open banking, a transformative approach that fosters collaboration between traditional banking institutions and third-party providers, is redefining the way consumers interact with their financial data. Meanwhile, the Dodd-Frank Act’s Section 1033 emerges as a crucial catalyst, empowering individuals to access and share their financial information with unprecedented ease and security. This article delves into the intricate relationship between open banking and Dodd-Frank 1033, exploring how these elements converge to unlock potential for consumers and innovators alike. By examining the implications of this evolution, we aim to shed light on the opportunities that lie ahead and the importance of navigating this complex landscape with insight and foresight. Join us as we unravel the intricacies of open banking and its regulatory underpinnings, and discover how they are poised to reshape the future of finance.

Exploring Open Banking: A Gateway to Financial Innovation

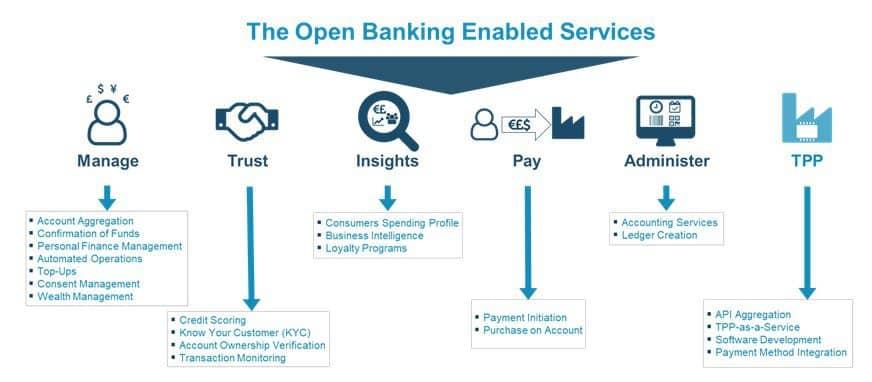

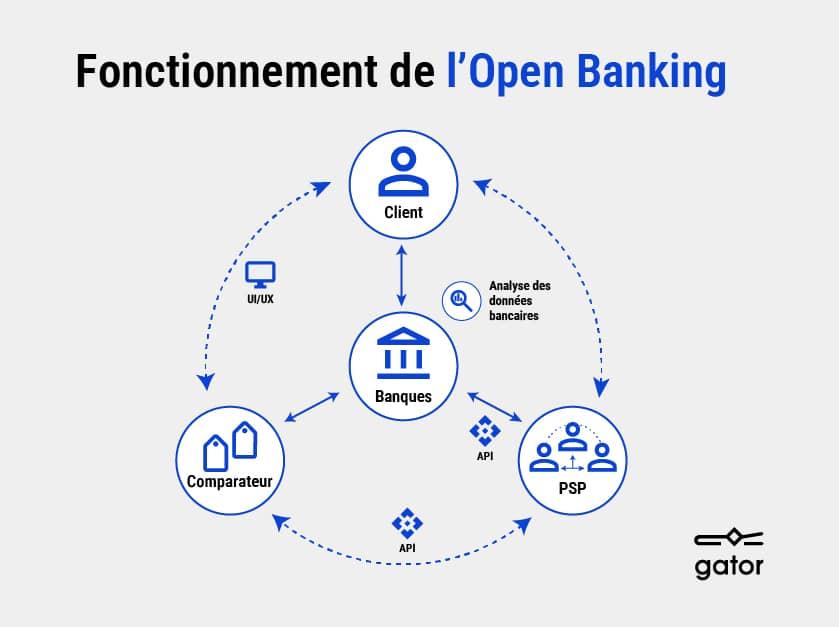

Open banking is transforming the financial landscape, creating a collaborative environment where banks, fintechs, and consumers can thrive. By utilizing APIs (Application Programming Interfaces), financial institutions can securely share customer data, spurring innovative services that meet diverse consumer needs. The implications of this evolution are vast, with possibilities ranging from personalized banking experiences to more competitive loan offerings. The implementation of Dodd-Frank Section 1033 underscores this shift by requiring financial institutions to share data with third-party providers, thereby fostering transparency and choice for consumers. This regulatory framework encourages healthy competition among banks and fintechs, ultimately benefiting customers.

The potential of open banking becomes increasingly apparent through its impact on various aspects of financial services. Here are some key innovations driven by this approach:

- Personal Finance Management Tools: Consumers can access apps that aggregate their financial information for better budgeting.

- Better Lending Options: Lenders can assess creditworthiness more accurately and offer tailored loan products.

- Seamless Payments: Enhanced payment experiences through instant transfers and reduced transaction fees.

This interconnected financial ecosystem not only empowers consumers with more control over their financial data but also encourages the development of cutting-edge solutions that enhance overall customer engagement. As this dynamic landscape evolves, staying ahead of the curve will be essential for financial institutions seeking to capitalize on the opportunities presented by open banking.

Understanding Dodd-Frank 1033: Balancing Safety and Accessibility

The Dodd-Frank Act, particularly Section 1033, aims to foster a financial ecosystem where consumers have unprecedented control over their financial data without compromising their security. This section establishes a framework that mandates financial institutions to enable customers to access their transaction histories and account information securely. In a world where data is the currency of innovation, embracing open banking principles can significantly enhance the customer experience by allowing third-party services to innovate on top of this data. However, this open access must be harmonized with robust security measures to ensure that consumers’ sensitive data is not only accessible but also well-protected against fraud and misuse.

Institutions face the challenge of striking the right balance between safety and accessibility. Key considerations include:

- Transparent Data Sharing: Ensuring consumers understand how their data is being used and shared with third parties.

- Robust Authentication Measures: Implementing advanced security protocols to protect consumer data from unauthorized access.

- Regular Compliance Audits: Conducting frequent reviews to ensure adherence to regulations while pursuing innovation.

To illustrate the implications of Dodd-Frank 1033 on consumer trust, consider the following:

| Aspect | Potential Impact |

|---|---|

| Consumer Empowerment | Increased control over personal financial data |

| Security Concerns | Heightened fear of data breaches |

| Market Innovation | Emergence of new financial products and services |

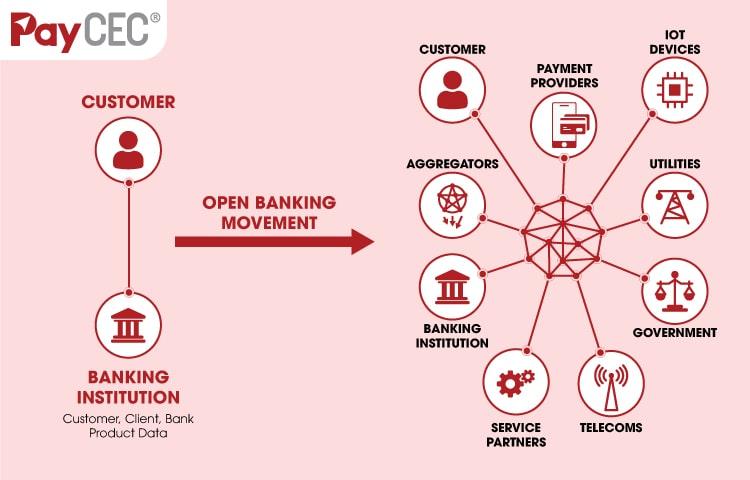

Empowering Consumers: The Role of Data Sharing in Financial Choices

The rise of digital financial services has transformed how consumers make decisions regarding their finances. With the implementation of open banking, individuals can now access a wider array of financial products tailored to their specific needs. By sharing their data across various financial platforms, consumers gain insights that were previously out of reach. This level of transparency not only enhances their understanding of their own financial health but also empowers them to compare options quickly, enabling informed decision-making. Some benefits of data sharing include:

- Personalized Recommendations: Financial institutions can provide services that better match individual consumers’ profiles.

- Competitive Offers: Consumers can easily evaluate multiple offers, which encourages fair pricing and better services.

- Improved Financial Literacy: Access to diverse financial products equips customers with knowledge that can lead to better financial management.

Additionally, the Dodd-Frank Act’s Section 1033 ensures that consumers have the rights to their financial data, enabling them to share this information with third-party providers. This legislation acts as a catalyst for innovation within the financial sector. Companies are incentivized to build applications and services that utilize consumer data securely and transparently. Consider the following attributes that define the benefits of Section 1033:

| Attribute | Description |

|---|---|

| Accessibility | Consumers can seamlessly access and share their financial information. |

| Security | Robust protections are in place to safeguard customer data. |

| Choice | More options for financial products lead to better consumer experiences. |

Strategic Recommendations for Navigating Open Banking Regulations

To effectively navigate the complexities of open banking regulations, financial institutions and third-party providers should adopt a proactive approach centered around a few strategic priorities. First, fostering a culture of compliance is essential, which involves integrating regulatory considerations into every aspect of the organization’s operations. Second, entities should invest in robust technology solutions that enhance data security and facilitate efficient data-sharing protocols with consumer consent. This not only ensures adherence to regulations but also builds customer trust and satisfaction.

Additionally, organizations must stay abreast of evolving regulatory landscapes by engaging in continuous education and collaboration with legal and compliance experts. Key actions include:

- Establishing a dedicated compliance team to monitor regulatory changes.

- Conducting regular training sessions for staff on open banking principles.

- Participating in industry forums to share insights and best practices.

developing transparent communication strategies with customers will empower them to make informed decisions regarding their financial data, thereby driving adoption of open banking services.

To Wrap It Up

as we stand on the cusp of a financial revolution, the intersection of Open Banking and the insights drawn from Dodd-Frank Section 1033 presents a transformative opportunity for consumers and institutions alike. By embracing transparency, fostering innovation, and prioritizing consumer empowerment, we unlock the vast potential of our financial ecosystem. As stakeholders navigate this evolving landscape, it becomes clear that the future of finance is not merely about transactions, but about establishing deeper, more meaningful relationships built on trust and accessibility. As we take these crucial steps forward, the promise of Open Banking beckons—a call to action for all to engage, innovate, and participate in crafting a more inclusive financial future. The journey is just beginning, and the possibilities are boundless.